CARES Act: Implications for Employers

By Michael J. Lotito, Jim Paretti, Alex MacDonald, Katy McConnell, Blaze Knott, McKinley Anderson, and Amanda Trull

NOTE: Because the COVID-19 situation is dynamic, employers should consult with counsel for the latest developments and updated guidance on this topic.

The Coronavirus Aid, Relief and Economic Security (CARES) was enacted on Friday, March 27, 2020. The CARES Act creates a half-dozen new programs to help distressed businesses and workers deal with COVID-19 and related shutdowns. These programs include forgivable loans, tax credits, and expanded unemployment insurance.

Paycheck Protection Program

First, the Act creates the Paycheck Protection Program, a new forgivable loan program to help small employers pay their expenses—and hold on to their workers—during the COVID-19 crisis.

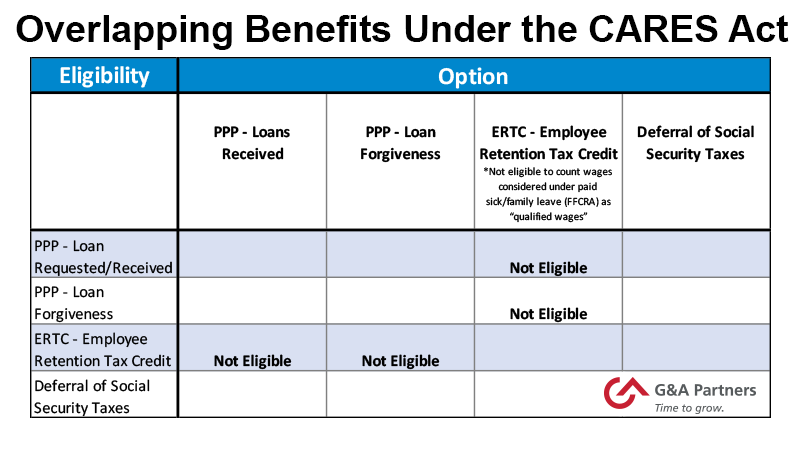

The Program provides loans of up to 250% of the employer’s average monthly payroll costs, with a cap of $10 million. Average monthly costs are determined by looking back one year from the date of the loan.1 An employer may use such a loan to cover salaries, group health benefits, rent, utilities, and other specified expenses. But the employer may not use the loan to pay for other coronavirus-related benefits, such as paid leave under the Families First Coronavirus Response Act (FFCRA).

Paycheck Protection loans are, however, available only to “small” employers. An employer qualifies as “small” if it employs fewer than 500 workers or fewer than the level set by the Small Business Administration (SBA) for the employer’s industry. These rules differ for some types of employers. For example, a hospitality or food services employer can qualify for a loan if it employs fewer than 500 workers per physical location. Franchised employers can disregard normal SBA affiliation rules, allowing them to more easily fall under the 500-employee threshold.

Congress gave the SBA responsibility for implementing the program. The SBA will make the loans available through existing lenders. It will also waive standard fees and personal-guarantee requirements—no collateral is required. Instead, the SBA will require employers to certify that: (1) the employer needs a loan to support its operations; (2) the employer will use the loan to retain its workers, maintain payroll, or pay other qualifying expenses; (3) the employer does not have another application for the same purpose pending; and (4) the employer has not already received a loan covering the same period.

A Paycheck Protection loan comes with a low interest rate—4% or less. These loans will be forgiven if the employer maintains its workforce for the covered period: February 15, 2020, to June 30, 2020. If the employer reduces its workforce during the covered period relative to last year, or reduces the salary or wages paid to an employee by more than 25%, the loan forgiveness will drop by the same percentage.

That means if an employer has already laid off employees or reduced their salaries, the Act offers less loan forgiveness. But the Act also allows an employer to avoid any reduction by rehiring employees or restoring their salaries. If the employer rehires all employees laid off since February 15, 2020, or increases employees’ previously reduced wages by no later than June 30, 2020, it is eligible for full forgiveness.

Direct Lending for U.S. Businesses

Second, the Act creates a $500 billion direct-lending program for U.S. businesses. This program includes emergency loans for general businesses, as well several special-assistance programs for key industries, like the airline industry. Businesses accepting the loans must also accept temporary limits on their ability to compensate executives and buy back stocks.

Within the larger program, the Act allows the treasury secretary to create a special loan program for mid-size businesses—i.e., those with 500 to 10,000 employees. Loans under this program accrue no interest for the first six months, and the recipient need not make any principal payments during that time. The recipient must, however, certify that it will meet certain conditions. For example, it must certify that it will use the loan to retain at least 90% of its workforce at full compensation and benefits until September 30, 2020. It must also certify that it intends to restore at least 90% of its workforce as of February 1, 2020—again, with full compensation and benefits. Other conditions include that, for the life of the loan, the recipient will not outsource jobs, will not abrogate any collective bargaining agreement, and will remain “neutral” in any union organizing effort.

How far these conditions reach remains to be seen. The Act states that the secretary of the treasury will “endeavor” to create the mid-size-loan program; it does not require him to create the program. Nor is it clear how many employers will apply for the mid-size loans, even if made available, given some of the conditions. In any event, those conditions apply only to the mid-size loans—they do not apply to the other direct loans.

Employee Retention Tax Credit

Third, the Act offers tax credits to employers that have seen their operations shuttered or partially shuttered because of COVID-19.

The credits can go as high as 50% of qualified wages paid to an employee between March 13, 2020, and the end of the year. These credits max out at $10,000 per employee. They also apply only to employment taxes, such as FICA, federal unemployment taxes, and Social Security taxes. And they cannot be taken alongside other coronavirus-related benefits, such as credits for paid leave under the FFCRA or Paycheck Protection loans.

To qualify for the credits, the employer must experience (a) a full or partial shutdown because of a government order related to COVID-19, or (b) a decline in revenues of 50% or more from the same period last year. Qualifying employers with 100 employees or fewer can take a credit for all qualifying wages. Larger companies with more than 100 employees can also take a credit, but only for wages paid to employees who are not working because of reasons (a) or (b).

Deferral of Payroll Taxes

Fourth, the Act allows employers to defer2 Social Security taxes. Any deferred payment would need to be paid over the next two years, with half due by December 31, 2021, and the rest due by December 31, 2022.

Expanded Unemployment Insurance3

Fifth, the Act pumps $250 billion dollars into the unemployment insurance system. These new benefits are available to nearly every employee displaced by COVID-19—and even to some not considered employees at all.

The Act expands benefits by raising the maximum payment across the board by $600 per week. That expansion alone works out to $15 an hour for a 40-hour week. The Act also extends benefits for 13 weeks beyond what states already allow.

Any employee unable to work because of COVID-19 can apply for the benefits. Some self-employed workers and independent contractors can also apply. Worker cannot apply, however, if they have the ability to telework. Nor can the worker apply while receiving other coronavirus-related benefits, such as paid leave under the FFCRA.

Many questions remain about these provisions. For example, it is not yet clear who decides when an employee can telework. And some have already expressed concerns about the Act’s potential negative incentives. By disconnecting weekly benefits from an employee’s earnings, the Act may make it possible for employees to earn more in unemployment benefits than they earn by working.

Immediate Tax Credits for FFCRA Leave

Sixth, the Act gives employers an immediate way to pay for leave under the FFCRA.

The FFCRA created two new paid-leave programs: (1) two weeks’ paid emergency sick leave, and (2) up to 12 weeks’ emergency family and medical leave, the first two weeks of which are unpaid, but as a practical matter, likely to be compensated by way of emergency paid sick leave. This leave is generally paid at the employee’s regular rate (or 2/3 of that rate for family leave), subject to certain dollar-value caps. The Act helps employers pay for those new benefits by providing an advance tax credit immediately, rather than recovering the money after paying.

Beyond that, it is not yet clear how the credits will be implemented. The Act gives the treasury secretary authority to implement the credits by regulation. More guidance is expected in the coming days.

Agencies like the Department of Labor, the Internal Revenue Service, and the Small Business Administration are working to provide guidance and procedures for many of these new programs. Indeed, the information available about all these programs changes daily, if not hourly. Because the Act raises complex and novel questions about interpretation and compliance, employers should consult with legal counsel. For employers seeking loans under the Act’s various new programs, it is especially important that they understand the programs’ rules and requirements before committing.

1 Seasonal employers use instead the period of February 15, 2019, to June 30, 2019.

2 The deferral period begins on the date the CARES Act was enacted and ends before January 1, 2021.

3See also William Hayes Weissman et al., Senate Passes CARES Act with Relief for Businesses and Additional Unemployment Benefits, Littler ASAP (Mar. 26, 2020).

PLEASE NOTE: This content has been provided by G&A's legal partner firm Littler Mendelson P.C., and is shared with their permission. This information is only a summary of what is included in the new legislation and should not be considered legal advice. If you are seeking to take action or contemplating action based on the Families First Coronavirus Response Act and the CARES Act, please consult with your legal counsel so that you and your counsel may consider all relevant facts particular to your business.